|

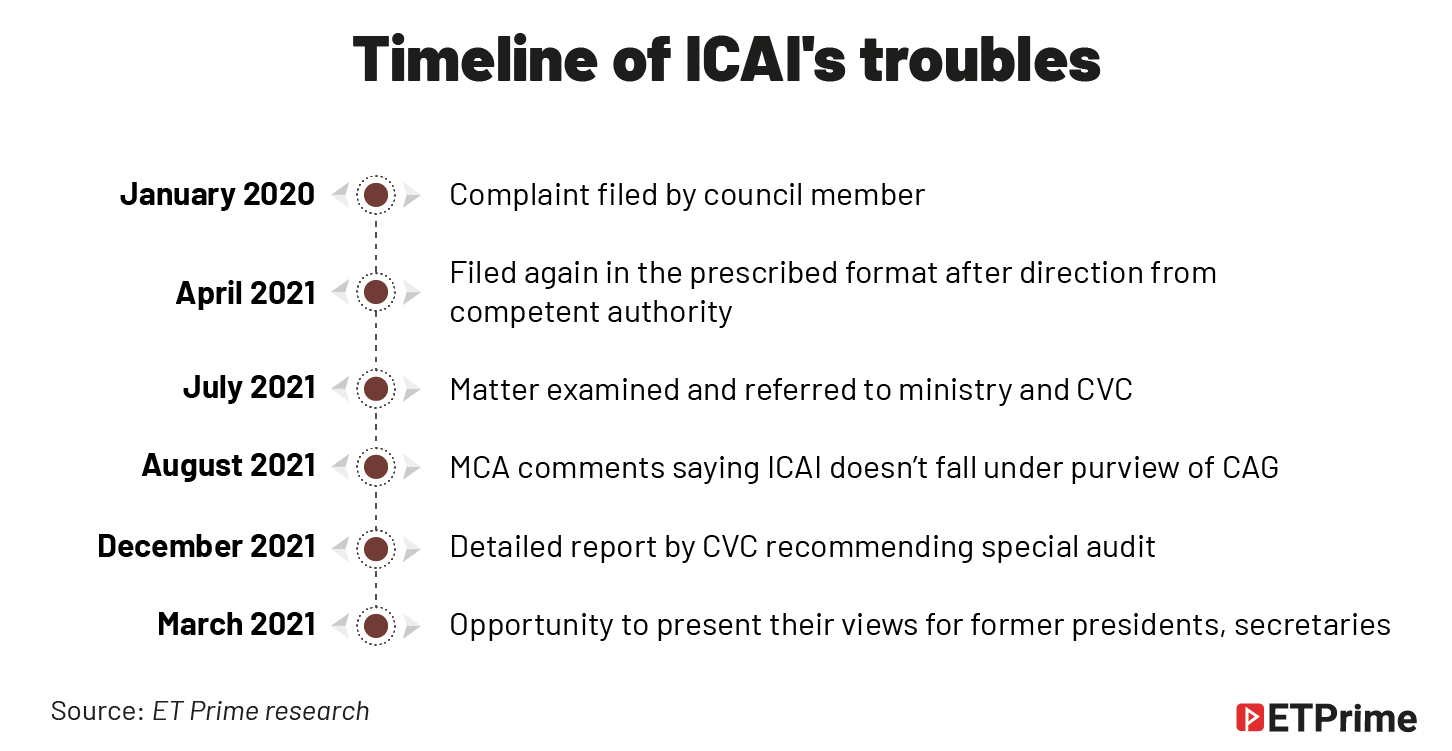

The Central Vigilance Commission (CVC) has recommended a special audit into the accounts of the Institute of Chartered Accountants of India (ICAI) by the national auditor, the Comptroller and Auditor General (CAG).

It has also asked for greater disclosures and transparency in the functioning of the institute. The recommendations come at a time when the parliamentary standing committee on finance is examining crucial amendments to the ICAI Act, 1949.

If accepted and implemented, these recommendations will go a long way in ushering in the much-needed reforms in the functioning of the ICAI, which is supposed to be the watchdog of the audit profession.

The recommendations came after CVC was asked to examine complaints of alleged financial irregularities in the institute in the years 2019-20 and 2020-21 during the tenures of former presidents Prafulla Chhajed and Atul Gupta, respectively.

The views of the Union Ministry of Corporate Affairs, which is the administrative ministry, had also been sought on the matter. Though the ministry opined that the institute is an autonomous body formed under an Act of Parliament and does not fall under the government, and therefore would not come under the purview of the national auditor, the CVC was of the view that the special audit might be considered for the relevant years given the gravity of the allegations.

Chhajed, Gupta and the secretaries of the institute during the respective periods have been asked to share their responses.

Complaint and recommendations

A former central council member, while he was still part of the council, had allegedly noticed several irregularities in foreign travel by the office-bearers, lack of transparency in work allotments and other instances of abuse of power and irregularities in the working of the institute.

However, in the president-centric functioning of the council, the voice of his dissent did not get a proper hearing. Following this, he escalated this matter through complaints to the ministry and other constitutional bodies.

The CVC is said to have provided detailed recommendations in tabular format going through each allegation in detail. It suggested several systemic improvements to address serious wrongdoing and deeply seated irregularities alleged by the complaints.

On the allegations of lack of transparency in accounts and other financial irregularities, the CVC said considering the gravity of the allegations, a special audit of the accounts by the office of CAG might be considered for the relevant years (2019-20, 2020-21). It also recommended adequate disclosures to be made in the notes of accounts of the audited financial statements.

Chhajed and Gupta did not respond to e-mails seeking comments.

An ICAI spokesperson says, “With regards to maintaining the accounts of ICAI, these are maintained in accordance with the provision of Regulation 194 of CA Regulations, 1988. Also, the finances of ICAI are dealt with in accordance with the provisions of Section 18 of the Chartered Accountants Act, 1949. The audit of accounts of the ICAI is done as per the provisions of Regulation 200 of CA Regulations, 1988 by independent firms of chartered accountants. Currently, the audit is carried out by two firms jointly.”

Senior members of the profession feel the entry of CAG will bring in a fresh approach and instill fear. According to them, CAs are by no means the ICAI’s only stakeholders. There are many others who are very important — such as students, the government, regulatory authorities, preparers and users of financial statements and other documents attested by CAs. So, the quality of the ICAI’s financial reporting and auditing are of great importance to a lot of external parties.

R Narayanaswamy, former professor of IIM-B and a CA himself, says he doesn’t like the idea of an auditee appointing the auditor. According to him, a fundamental requirement for auditor independence is that the auditor be appointed by a person or body other than the auditee. “This is the foundation on which trust in auditing is built.”

In ICAI’s case, the council appoints the auditor. In the past, the ICAI has campaigned for public-sector bank auditors to be appointed by the Reserve Bank of India and not by the banks’ boards of directors on the ground that appointment by the boards does not assure auditor independence.

“Leaving aside the merits of that argument, if that’s the principle they believe in, should they not lead by example and have their auditor appointed by an outside agency?” Narayanaswamy asks.

He adds that there was a further complication in the current arrangement. “The ICAI has disciplinary jurisdiction over CAs, including its auditors. So, there’s a conflict of interest in being an auditee and a disciplinary authority at the same time. If there are complaints about its financial statements or the audit quality, should the ICAI investigate the matter itself? That would be absurd,” Narayanaswamy says.

“At present, the auditors (of ICAI) approach it more as a compliance. If CAG comes, it will look into the accounts from a different perspective. It will bring an investigative and professional approach. This will instill fear in the minds of people who might want to abuse or misuse. This fear is not there at present,” says Anand Drolia, a Mumbai-based fellow member of the institute.

Narayanaswamy agrees, “I believe the ICAI’s financial statements should be audited by the CAG. After all, the ICAI is not a private organisation. It’s a statutory authority and it already comes under the Central Vigilance Commission and the Central Information Commission. Therefore, why not strengthen its accountability by bringing it under the CAG? The ICAI should lead by example by voluntarily opting to have a CAG audit, even though the law doesn’t require it. That would send a message that it has nothing to hide and it’s sincere.”

It is the lack of fear and accountability that allows the ICAI office-bearers to splurge crores in business class foreign travel, members feel.

Frequent fliers of ICAI

The CVC observed that ICAI did not have a clear policy or guidelines for travel entitlements of the office-bearers. To maintain transparency, the guidelines need to mention the entitlements of the council members, the commission has said. In FY20, before Covid-19 pandemic hit travel, the ICAI spent INR26.5 crore in travel, of this about INR2.3 crore was “overseas travelling”. In the following year, when travel curbs came into force, the institute’s travel bills came down to INR7.94 crore. There were no expenses on account of overseas travel in FY21.

Justifying the need for frequent foreign visits by the president and other office-bearers, the ICAI spokesperson said the ICAI representatives need to undertake overseas travel from time to time in order to present the viewpoint of the Indian Chartered Accountancy profession at global forums; to promote CA international curriculum abroad, to maintain audit quality on a par with global standards, to maintain a continuous dialogue with leading foreign accounting bodies; to initiate steps for recognition of Indian qualification abroad by entering into MoUs/MRAs and strengthen the interface between the institute and the members abroad.

“The travel of ICAI representatives is according to the proposal of the Central Council of ICAI. The council of ICAI fixes the travel allowances as per clause (d) of sub-section (2) of Section 16 of the Chartered Accountants Act, 1949 and in accordance with the approval of the central government. Hence, the council of ICAI is empowered to fix on its own, the allowances for the purpose of domestic and overseas travel. Also, the TA/ DA rules for domestic and overseas travel by ICAI representatives are approved by the Central Government vide its letters dated April 24, 2008, May 16, 2008 and November 5, 2015 respectively,” the spokesperson adds.

Lack of transparency

The CVC observed that the institute should put out important policy decisions in the public domain. It advised the institute to share the accounts and detailed agenda of all the council meetings in the public domain.

Members say though minutes of the council meetings are shared when applied through RTI, this is not consistent.

“Minutes are not shared. Only when you ask through RTI, they share it. They try to delay and give technical reasons when they do not want to reply. The (RTI) Act is strict. You can say they answer about 80% of the time,” Drolia adds.

The issue of allocation of work related to the restatement of accounts of IL&FS, the giant infrastructure conglomerate that crumbled in 2018, was also among matters under the CVC scrutiny.

The ICAI spokesperson says, “For other queries forwarded by you, there is no final outcome as yet.”

Sources close to the institute say the matters pertain to past years and the new dispensation that has taken charge last month, with president Debashis Mitra and vice-president Aniket Talati, is keen to turn a new leaf, bringing in transparency and putting stakeholders’ interest ahead of the internal politics.

How they navigate the tricky proposal of CAG audit would determine their course ahead. - (Source Economic Times)

|