How RBI’s New Digital Lending Rules Are Impacting Banks & NBFCs

India’s digital lending sector has grown rapidly over the last few years, driven by fintech innovation, mobile apps, and instant loan approvals. However, the rapid expansion also brought concerns such as hidden charges, unethical recovery practices, misuse of customer data, and unregulated loan apps. To address these issues, the Reserve Bank of India (RBI) introduced stricter digital lending guidelines aimed at increasing transparency, protecting borrowers, and strengthening accountability across the financial ecosystem.

The new framework is significantly reshaping the way banks, Non-Banking Financial Companies (NBFCs), and fintech partners operate in the digital lending market.

Why RBI Introduced New Digital Lending Rules

The RBI observed growing complaints related to digital lending platforms, including:

- Hidden processing fees and unclear interest rates

- Aggressive recovery methods

- Misuse of personal and financial data

- Fake and unauthorized lending apps

- Lack of transparency in loan agreements

To improve trust and ensure responsible lending practices, the regulator introduced revised digital lending directions for banks, NBFCs, and Lending Service Providers (LSPs).

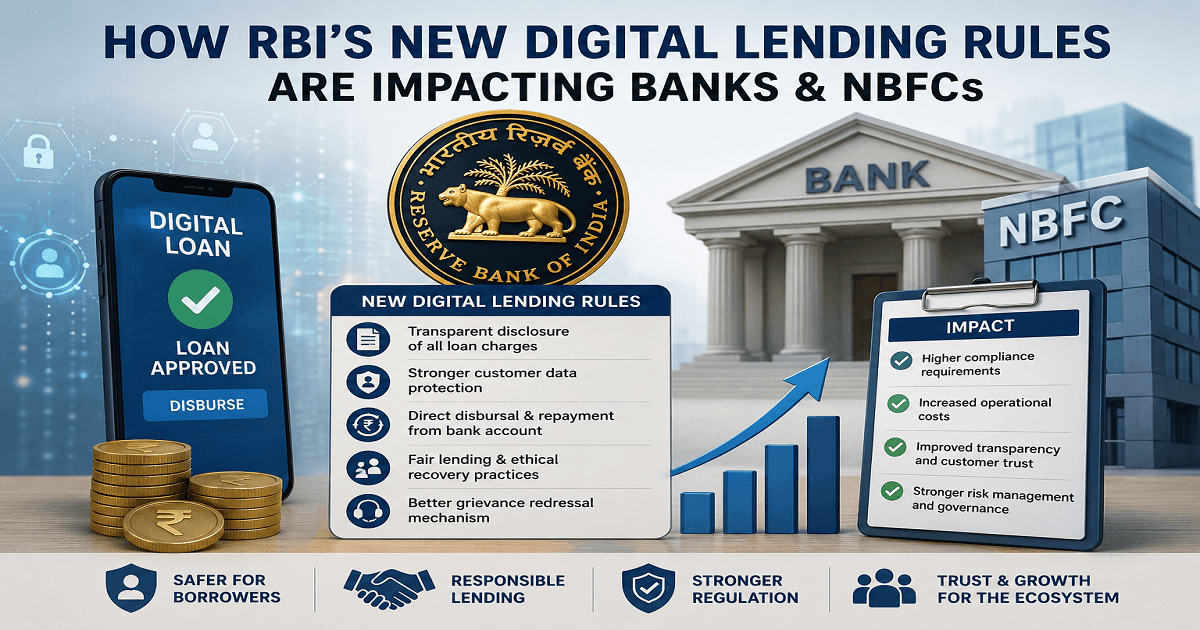

Key Highlights of RBI’s Digital Lending Guidelines

1. Mandatory Transparency in Loan Charges

Under the new rules, lenders must provide a clear Key Fact Statement (KFS) before loan disbursal. The KFS includes:

- Annual Percentage Rate (APR)

- Processing fees

- Penalty charges

- Total cost of borrowing

- EMI structure

This prevents hidden charges and helps borrowers make informed decisions.

2. Direct Loan Disbursal and Repayment

The RBI has mandated that all loan disbursals and repayments must happen directly between the borrower’s bank account and the regulated entity. Third-party pass-through accounts are restricted.

3. Stricter Rules for Lending Apps

Digital lending apps must now comply with stronger disclosure norms, data privacy requirements, and grievance redressal systems. Unauthorized apps and misleading lending practices are under tighter regulatory scrutiny.

4. Borrower Protection Measures

The RBI has also introduced measures such as:

- Cooling-off periods for certain loans

- Better customer consent mechanisms

- Transparent collection practices

- Enhanced KYC and verification standards

These changes aim to reduce predatory lending and improve customer confidence in digital finance.

Impact on Banks

Improved Compliance Requirements

Banks now need stronger compliance systems, cybersecurity frameworks, and monitoring mechanisms. Institutions offering digital banking services must ensure robust governance and customer protection standards.

Higher Operational Costs

Implementing advanced compliance systems, fraud monitoring, and data security infrastructure has increased operational costs for banks. Many banks are investing heavily in technology upgrades and risk management tools.

Better Customer Trust

Although compliance costs are rising, the rules are helping banks build stronger customer trust through transparent lending practices and improved grievance handling.

Changes in Fintech Partnerships

Banks are becoming more selective about partnering with fintech companies and digital lending service providers. Regulatory accountability now remains with the regulated entity, even when third-party platforms are involved.

Impact on NBFCs

Increased Regulatory Pressure

NBFCs, especially fintech-focused lenders, are facing tighter scrutiny regarding loan pricing, data handling, and customer onboarding practices.

Shift Towards Responsible Lending

Many NBFCs are redesigning their lending models to align with RBI standards. This includes clearer disclosures, ethical recovery practices, and better risk assessment methods.

Compliance Burden for Smaller NBFCs

Smaller NBFCs and fintech startups may struggle with the increased cost of compliance, technology integration, and legal requirements. Some smaller players could exit the market or merge with larger institutions.

Stronger Market Credibility

For compliant NBFCs, the new framework creates long-term advantages by improving investor confidence and borrower trust.

Impact on Borrowers

The biggest beneficiaries of the RBI’s digital lending reforms are borrowers. Customers now receive:

- Greater transparency in loan pricing

- Better protection from fraud and harassment

- Improved data privacy safeguards

- Faster grievance resolution mechanisms

- Safer and more reliable lending platforms

The rules also help borrowers identify legitimate RBI-regulated lenders more easily.

Challenges Ahead

Despite the positive impact, challenges remain:

- Increased compliance costs for lenders

- Slower loan approval processes in some cases

- Reduced profitability for certain high-risk lending models

- Need for continuous cybersecurity upgrades

The digital lending ecosystem is still evolving, and financial institutions will need to balance innovation with regulatory compliance.

Conclusion

RBI’s new digital lending rules mark a major shift toward a safer, more transparent, and borrower-centric financial ecosystem in India. While banks and NBFCs may face higher compliance costs and operational adjustments, the long-term benefits include improved credibility, reduced fraud risks, and stronger consumer confidence.

As digital lending continues to grow, these regulations are expected to create a more sustainable and trustworthy financial environment for lenders, fintech companies, and borrowers alike.

Category : RBI | Comments : 0 | Hits : 687

Comments