New Income Tax Act 2025: Key Changes and Benefits for Individuals

The Income Tax Act, 2025, set to come into force from April 1, 2026, will replace the long-standing Income Tax Act, 1961. The new law aims to simplify the tax system, improve transparency, and reduce compliance burden for taxpayers by introducing a more streamlined framework.

One of the major highlights is the consolidation of forms and provisions. The earlier structure, which consisted of 819 sections and 14 schedules, has been significantly reduced to 536 sections and 16 schedules. Similarly, rules have been cut down from 511 to 333, and the number of forms has been almost halved from 390 to 190, making the system more user-friendly.

A notable change for individual taxpayers is the merging of Form 15G and Form 15H into a single Form 121. Earlier, taxpayers had to choose between these forms based on age, often leading to confusion. The new unified form removes this distinction and can be used by all eligible individuals, including HUFs and specified entities, to declare nil taxable income and avoid unnecessary TDS deductions.

Another key improvement is that taxpayers will now be able to submit a single Form 121 across multiple financial institutions, instead of filing separate forms for each account. This will be supported by a single identification number, reducing duplication and the risk of excess TDS.

In addition, Form 26AS has been renamed as Form 168 and expanded in scope. The new form acts as a comprehensive financial statement, integrating details from the Annual Information Statement (AIS). It will provide a complete overview of a taxpayer’s financial activities, including income, investments, and high-value transactions, offering better visibility and accuracy.

The Act also brings relief under the Liberalised Remittance Scheme (LRS) by reducing TCS rates. For education, medical expenses, and overseas tour packages exceeding ₹10 lakh, the TCS rate has been lowered from 5% to 2%, easing the upfront tax burden on individuals.

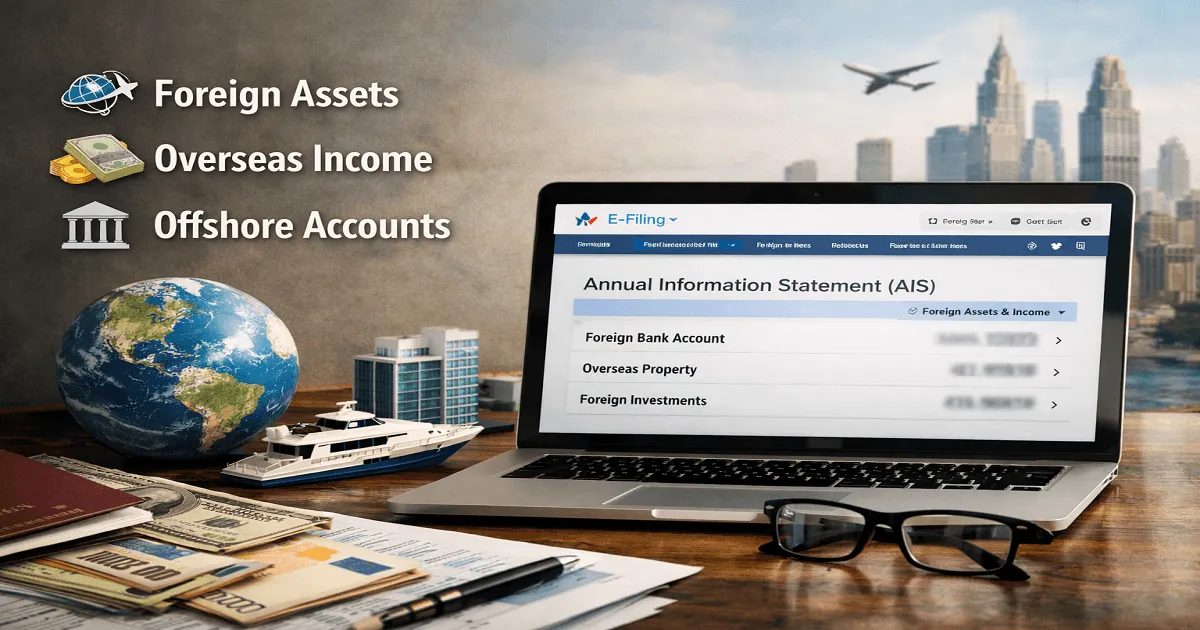

Further, the introduction of the FAST Disclosure Scheme (FAST-DS 2026) offers a limited-time opportunity for taxpayers to voluntarily disclose undisclosed foreign assets or income. This scheme is particularly beneficial for small taxpayers, allowing them to regularize their records at lower tax rates and avoid strict penalties.

Overall, the Income Tax Act, 2025 reflects a shift towards a more simplified, technology-driven, and taxpayer-friendly system, focusing on ease of compliance and better financial transparency.

One of the major highlights is the consolidation of forms and provisions. The earlier structure, which consisted of 819 sections and 14 schedules, has been significantly reduced to 536 sections and 16 schedules. Similarly, rules have been cut down from 511 to 333, and the number of forms has been almost halved from 390 to 190, making the system more user-friendly.

A notable change for individual taxpayers is the merging of Form 15G and Form 15H into a single Form 121. Earlier, taxpayers had to choose between these forms based on age, often leading to confusion. The new unified form removes this distinction and can be used by all eligible individuals, including HUFs and specified entities, to declare nil taxable income and avoid unnecessary TDS deductions.

Another key improvement is that taxpayers will now be able to submit a single Form 121 across multiple financial institutions, instead of filing separate forms for each account. This will be supported by a single identification number, reducing duplication and the risk of excess TDS.

In addition, Form 26AS has been renamed as Form 168 and expanded in scope. The new form acts as a comprehensive financial statement, integrating details from the Annual Information Statement (AIS). It will provide a complete overview of a taxpayer’s financial activities, including income, investments, and high-value transactions, offering better visibility and accuracy.

The Act also brings relief under the Liberalised Remittance Scheme (LRS) by reducing TCS rates. For education, medical expenses, and overseas tour packages exceeding ₹10 lakh, the TCS rate has been lowered from 5% to 2%, easing the upfront tax burden on individuals.

Further, the introduction of the FAST Disclosure Scheme (FAST-DS 2026) offers a limited-time opportunity for taxpayers to voluntarily disclose undisclosed foreign assets or income. This scheme is particularly beneficial for small taxpayers, allowing them to regularize their records at lower tax rates and avoid strict penalties.

Overall, the Income Tax Act, 2025 reflects a shift towards a more simplified, technology-driven, and taxpayer-friendly system, focusing on ease of compliance and better financial transparency.

Category : Income Tax | Comments : 0 | Hits : 54

Comments