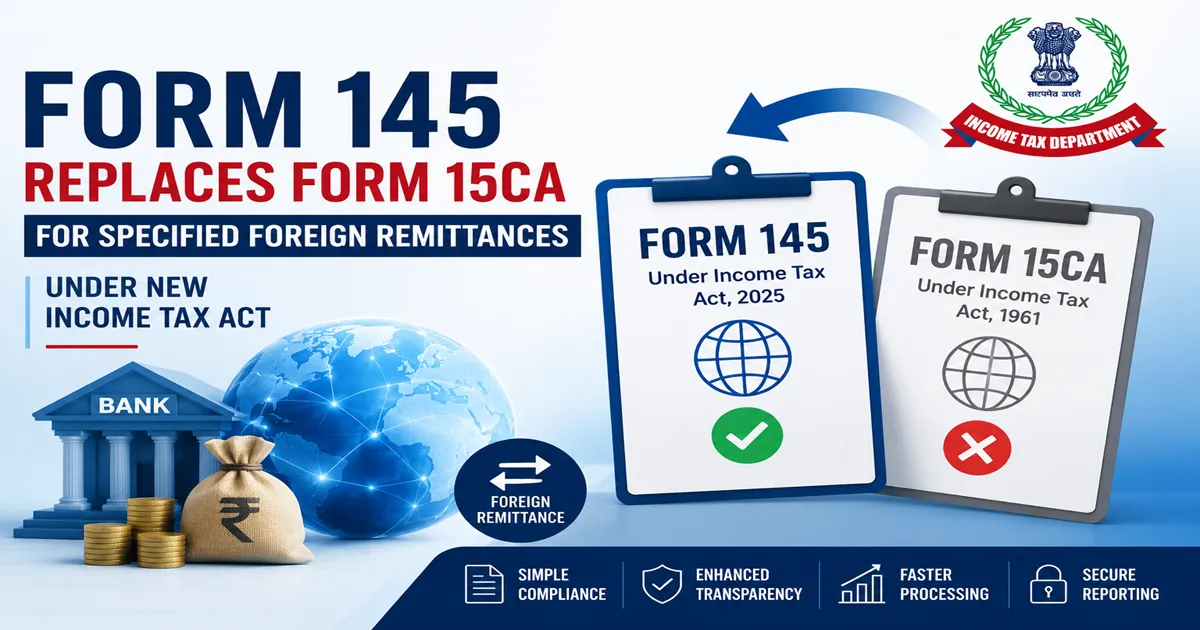

Form 145 Replaces Form 15CA for Foreign Remittances Under New Income Tax Act

The Income Tax Department has introduced Form No. 145, replacing the existing Form 15CA for reporting specified foreign remittances under the Income Tax Act, 2025. The new form is applicable for remittances governed by the new tax framework and aims to simplify compliance while strengthening reporting requirements for cross-border payments.

The change forms part of the transition from the Income Tax Act, 1961 to the Income Tax Act, 2025, which came into effect from 1 April 2026. The Income Tax Department has also issued a detailed user manual and Frequently Asked Questions (FAQs) to assist taxpayers and professionals in understanding the new compliance framework.

What is Form 145?

Form No. 145 is a statutory declaration that must be furnished before making specified payments to a non-resident or a foreign company. Similar to the earlier Form 15CA, it enables the Income Tax Department to monitor foreign remittances and ensure compliance with India's tax deduction at source (TDS) provisions.

The form is filed electronically through the Income Tax e-Filing Portal before the remittance is processed by the authorised dealer bank.

Why Has Form 15CA Been Replaced?

The replacement is part of the implementation of the Income Tax Act, 2025 and the Income Tax Rules, 2026.

Besides renumbering the form, the Department has updated the reporting structure to align it with the provisions of the new law. The objective is to simplify the remittance process while capturing more structured information required under the new income-tax framework.

Structure of Form 145

Like the earlier Form 15CA, Form 145 contains different parts depending on the nature and value of the remittance.

According to the official FAQs:

- Part A – Applicable where the remittance is chargeable to tax and the aggregate amount does not exceed ₹5 lakh during the Tax Year.

- Part B – Applicable where a certificate or order has been obtained from the Assessing Officer.

- Part C – Applicable where the remittance is taxable and exceeds ₹5 lakh during the Tax Year. In such cases, a Chartered Accountant's certificate in Form 146 (replacing Form 15CB) is generally required.

- Part D – Applicable where the remittance is not chargeable to tax or falls under specified exempt categories.

Form 146 Replaces Form 15CB

Another important procedural change is the replacement of Form 15CB with Form 146.

Where a Chartered Accountant's certification is required, the CA will now issue Form 146 instead of Form 15CB under the new Act. The certificate confirms the nature of the payment, taxability, applicable withholding tax and compliance with the provisions of the Income Tax Act, 2025.

Filing Process

The Income Tax Department has provided the following broad process for filing Form 145:

- Log in to the Income Tax e-Filing Portal.

- Navigate to e-File → Income Tax Forms.

- Select Forms as per Income Tax Act, 2025.

- Choose Form No. 145.

- Complete the relevant part of the form based on the nature of the remittance.

- Where applicable, obtain the CA-certified Form 146 before filing Part C.

- Submit the form electronically before making the remittance.

Can Form 145 Be Withdrawn?

The official user manual states that a filed Form 145 can be withdrawn within the prescribed period if the remittance is not ultimately made or the transaction requires correction. Taxpayers should review the latest portal instructions and applicable conditions before exercising this option.

Impact on Taxpayers and Chartered Accountants

The introduction of Form 145 is expected to affect:

- Individuals making overseas remittances;

- Businesses making payments to non-residents or foreign companies;

- Banks and authorised dealers processing remittances;

- Chartered Accountants certifying taxable remittances; and

- Tax professionals advising on international tax compliance.

CA firms may also need to update internal checklists, SOPs, software mappings and client advisory documents to reflect the replacement of Forms 15CA and 15CB with Forms 145 and 146 respectively.

Key Takeaway

The introduction of Form 145 marks an important procedural change under the Income Tax Act, 2025. While its core objective remains similar to the erstwhile Form 15CA—reporting specified foreign remittances—the new form aligns the reporting mechanism with the provisions of the new income-tax law.

Taxpayers making payments to non-residents and foreign companies should ensure that the correct part of Form 145 is filed before remitting funds and, where required, obtain the corresponding Chartered Accountant's certificate in Form 146. Professionals should also monitor further notifications and operational guidance issued by the Income Tax Department as the new compliance framework continues to evolve.

Category : Income Tax | Comments : 0 | Hits : 60

Comments